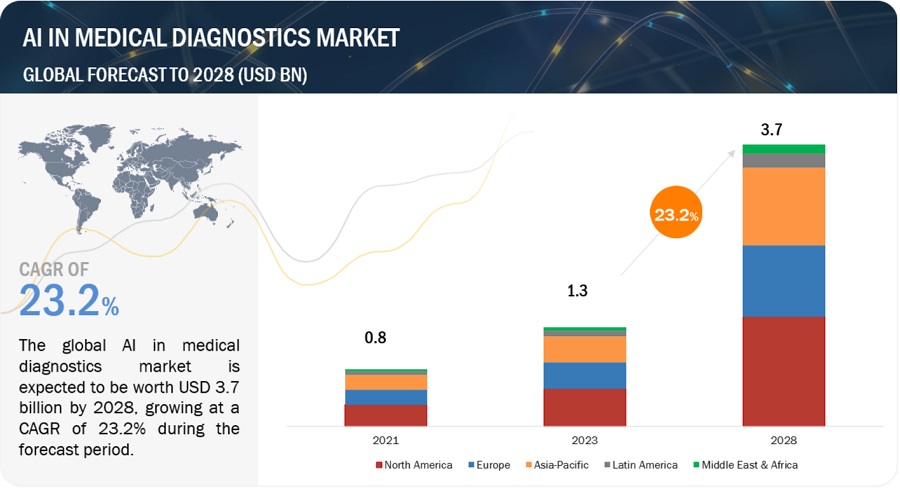

Artificial Intelligence (AI) in Medical Diagnostics Market, valued at $1.3 billion in 2023, is expected to surge to $3.7 billion by 2028, with a CAGR of 23.2%. This analysis focuses on industry trends, pricing models, patents, and key market stakeholders, including insights on buying behaviors and industry events.

Download an Illustrative overview

“Software segment is estimated to account for the largest share of the AI in Medical Diagnostics Market in 2023, by component”

On the basis of components, the AI in medical diagnostics market is segmented into software, hardware, and services. In 2023, the software segment is expected to hold the largest share of this market, while the software segment is estimated to grow at a higher CAGR from 2023 to 2028. Software solutions empower healthcare providers to maintain a competitive edge, even in the face of challenges such as staffing shortages and the growing volume of imaging scans.

“The In Vivo Diagnostics segment is estimated to account for the largest share of the AI in Medical Diagnostics Market in 2023, by application”

On the basis of application, AI in medical diagnostics market is divided into in vivo and in vitro diagnostics. In 2023, the in vivo diagnostics segment is expected to hold the largest share of this market. Factors such as rising adoption of AI solutions by practitioners, as these solutions aid lower human errors and advance treatment efficacy. However, the in vitro diagnostics segment is estimated to register highest CAGR during forecast period. In Vitro diagnostics is conducted mainly conducted in diagnostic laboratories, pathologies, microbiology centers, and immunology centers. However, in Vitro diagnostics has high growth potential,as it is largely untapped, especially in emerging markets.

“The Hospital segment is estimated to account for the largest share of the AI in Medical Diagnostics Market in 2023, by end user”

On the basis of end users, AI in medical diagnostics market is segmented into hospitals, diagnostic imaging centers, diagnostic laboratories, and other end users. In 2023, the hospitals segment is expected to hold the largest share of this market. Growth in this segment is driven by rising use of minimally invasive processes in hospitals to focus on quality of patient care, and the mounting adoption of advanced imaging modalities to improve workflow efficiency.

“North America to dominate the AI in medical diagnostics market in 2023”

On the basis of region, AI in medical diagnostics market has been segmented into North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2023, North America is projected to account for the largest market share of this market. However, the Asia Pacific market is projected to register the highest CAGR during the forecast period. The high growth rate of the Asia Pacific market can be due to expanding number of cancer patients in Asia Pacific countries and growth approaches companies implement in emerging markets.

Artificial Intelligence (AI) in Medical Diagnostics Market Dynamics:

Drivers:

- Influx of big data

- Growing number of cross-industry partnerships & collaborations

- Increasing demand for AI-based solutions to reduce work pressure on radiologists

- Rising government initiatives to drive AI-based technologies

- Availability of funding for AI-based startups

Restraints:

- Reluctance among medical practitioners to adopt AI-based technologies

- Inadequate AI workforce and ambiguous regulatory guidelines for medical software

Opportunities:

- Untapped emerging markets

- Growing potential of AI in imaging diagnostics for COVID-19

- Increasing focus on developing human-aware AI systems

Challenge:

- Budgetary constraints

- Unstructured healthcare data

- Data privacy concerns

- Limited interoperability for AI solutions

Key Market Players of Artificial Intelligence (AI) in Medical Diagnostics Industry:

Prominent players in AI in Medical Diagnostics market are Microsoft (US), NVIDIA Corporation (US), Merative (US), Intel Corporation (US), Google (US), Siemens Healthineers (Germany), GE HealthCare (US), Digital Diagnostics Inc. (US), Advanced Micro Devices, Inc. (US), InformAI (US), HeartFlow, Inc. (US), Enlitic, Inc. (US), icometrix (Belgium), Aidence (Netherlands), Butterfly Network, Inc. (US), Nano-X Imaging LTD. (Israel), Viz.ai, Inc (US), Quibim (Spain), Qure.ai (India), Therapixel (France), Aidoc (US), Koninklijke Philips N.V. (Netherlands), Lunit, Inc. (South Korea), EchoNous, Inc. (US), and Brainomix (UK).

Get 10% Free Customization on this Report

Recent Developments:

- In September 2023, Mayo Clinic (US) and GE HealthCare (US) collaborated on research and product development programs to better equip clinicians and help diagnose and treat medical conditions.

- In January 2023, Intel Corporation (US) launched 4th Gen Intel Xeon Scalable processors (code-named Sapphire Rapids), the Intel Xeon CPU Max Series (code-named Sapphire Rapids HBM) and the Intel Data Center GPU Max Series (code-named Ponte Vecchio), delivering a leap in data center performance, efficiency, security and new capabilities for AI, the cloud, the network and edge, and the world’s most powerful supercomputers.

- In October 2022, Google Cloud (US) launched Medical Imaging Suite, a new industry solution that makes imaging healthcare data more accessible, interoperable, and useful. Google Cloud enables the development of AI for imaging to support faster, more precise diagnosis of images, increased productivity for healthcare workers, and improved care access and patient outcomes.

- In January 2022, Siemens Healthineers (Germany) and Ohio State Wexner Medical Center (US) partnered to provide cutting-edge imaging and treatment technology to Ohio State patient care, research institutions, and the surrounding regions. The alliance offers cutting-edge radiation oncology and advanced imaging modalities on the Outpatient Care West Campus.

Content Source:

https://www.marketsandmarkets.com/PressReleases/artificial-intelligence-medical-diagnostics.asp